Digital Distress

Fidelity Spars with DOL Over Crypto: No Asset for Nest Eggs

There is a whiff of distress in cryptoland.

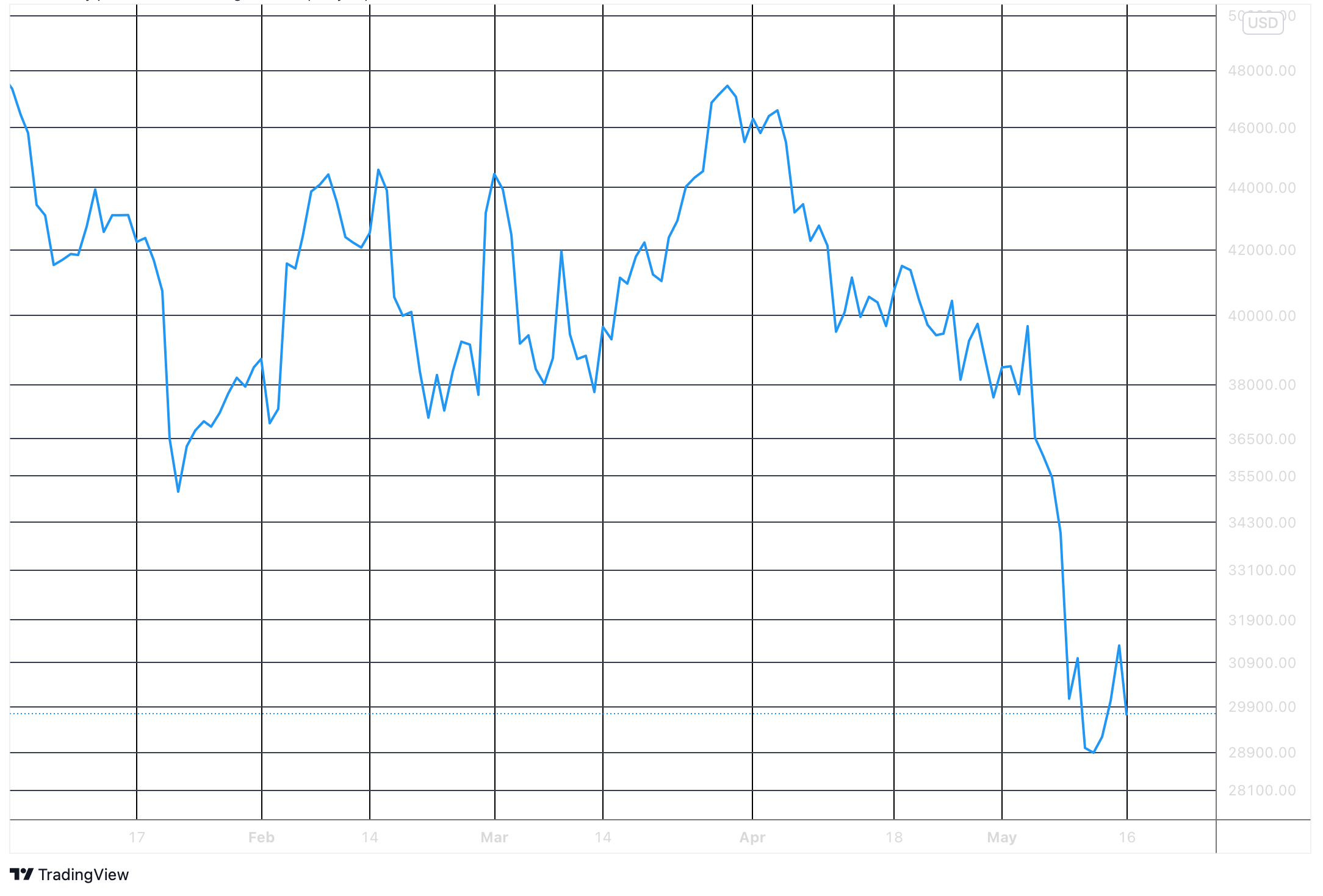

Bitcoin is trading under $30,000, down 55% from its high.

Coinbase Global, the biggest U.S. crypto exchange, posted a quarterly loss of $430 million thanks to plummeting trading volume.

A supposedly “stable” coin, TerraUSD, collapsed to near zero.

Perhaps the most foreboding news: a U.S. regulator threw a serious kink in the crypto industry’s efforts, led by Fidelity Investments, to go after American retirement savings. More on that to come.

Crypto was supposed to be a hedge against inflation, yet even as the dollar buys less in groceries and gasoline its value in crypto is soaring. Why is that?

Crypto is the ultimate yield-free asset—no dividends, no interest payments, no cash flow, no revenue.

That was OK, sort of, as long as the Federal Reserve distributed dollars for free. Speculating in crypto cost virtually nothing. You could fill your yard with rocks (on credit) and that cost nothing, too.

Roughly in November (when bitcoin peaked), the Fed said no mas. Money henceforth would carry a cost.

No one knows how high interest rates will go, but for most of recorded history the cost of money has been higher than the inflation rate (otherwise, why would lenders lend?)

The last decade was an anomaly—lenders settling for negative real returns. That era is vanishing if it isn’t already over. In plain math, why lend at 3%, or 4%, if inflation is 8%. Even if inflation were to fall in half, lending at present rates would yield a negative real return.

The bond market had been asleep to such calculations, but inflation has roused it. As rates rise, the value of investments perforce falls. Investments with fixed yields suffer the most, and those with yields fixed at zero suffer the very most. Andy Warhol’s platinum-yellow “Shot Sage Blue Marilyn” recently sold for less than half of what had been forecast. Warhols yield as much as bitcoin (nothing), but unlike crypto, they at least look good on a wall. If the monetary cycle has turned, crypto could be the first casualty.

Prices fluctuate and we assume that will true be of bitcoin’s. But it is worth pointing out that more than a decade into the crypto era, bitcoin, in the words of Eswar Prasad, the Cornell University trade policy and economics professor and author of “The Future of Money,” has become a

pure speculative asset whose whole value is based on scarcity. The design is clever, a cap of 21 million coins coded by the creator, of which about 19 million are created so far. The notion of [scarcity] seems to underline investment faith. To an economist, the idea of scarcity alone is not sufficient. Investors are being taken in by the razzle dazzle of newness.

A similar revulsion to razzle-dazzle—one might call it prudence—seems to have struck the Department of Labor. Not waiting for the bubble to pop, in March DOL issued a blistering “compliance assistance release” warning of its concern with firms planning to offer cryptocurrencies as an option in 401(k) retirement plans.

DOL has no stake in how Americans invest, or speculate with, taxable assets. It has, however, a vested interested in assuring that the estimated (as of the end of 2021) $8 trillion in 401(k) plans are managed with prudence.

Retiree savings are not only a personal but also a societal asset, shielded from taxation for the purpose of securing some minimum comfort for retirees. A meltdown in retirement savings would present a social crisis on a par with the late mortgage debacle. According to the Federal Reserve, in 2019 the median 401(k) held $65,000, presumably, not enough to a “prudent man” to warrant gambling.

DOL has not asserted authority to block 401(k) providers from offering crypto. What it did do was to put fiduciaries on notice.

Under the ERISA statute, plan fiduciaries must act solely in the interest of participants (individuals) and adhere to an exacting standard of professional care. As DOL pointed out, courts have deemed the prudence and loyalty obligations of fiduciaries the “highest known to the law.”

Spelling out its concern, DOL noted that fiduciaries cannot shift responsibility to plan participants to identify and avoid imprudent choices. Rather, fiduciaries “must evaluate the designated investment alternatives made available and take appropriate measures to ensure that they are prudent.”

DOL voiced “serious concerns about the prudence” of exposing 401(k) money to crypto. It worries about its speculative nature, volatility, the difficulty of making an informed investment decision, the risk of lost passwords or theft.

DOL also aired a phrase usually avoided by regulators: “valuation concerns.” It noted with devastating clarity, “none of the proposed models for valuing cryptocurrencies are as sound or academically defensible as traditional discounted cash flow analysis for equities or interest and credit models for debt.” No cash flow, no valuation.

DOL did not name names, but it was aware that Fidelity, which administers $2.7 trillion in 401(k) money, plans to let sponsors include bitcoin on their menus of investment options for up to 20% of portfolios.

Ali Khawar, acting assistant secretary for DOL’s Employee Benefits Security Administration, told me that over the past year, as his division became aware of such plans, he asked potential marketers about valuation. “We did not hear any coherent theory on how to value it,” he said.

I asked Khawar whether, or how, he would distinguish the suitability of crypto from that of gold or art. He said one difference was the hype. “I don’t remember seeing celebrity endorsements on the Super Bowl about investing in rare art. A lot of … promotional materials [were] one-sided.” They “don’t educate people on the risks.”

Perhaps he meant Tom Brady or Larry David, who have shilled for the crypto industry. But he could have meant the promotional materials of Fidelity itself. A July 2020 research effort by the then-research director of Fidelity Digital Assets, still on the company’s website last week, touted crypto in devotional terms.

Bitcoin, if offered, is an “aspirational store of value.” Alluding to “debates” on whether bitcoin was a store of value, a medium of exchange, an alternative asset, or all or none of the above, Fidelity, sounding as smitten as Timothy Leary on the properties of lysergic acid diethylamide, advanced the proposition that “as the ecosystem matures, Bitcoin may simultaneously serve many functions – either foundationally or through incremental layers.” It reverently elaborated, “One of the beautiful things about Bitcoin is that its success is not predicated on serving a singular purpose.”

The Fidelity research, penned when the price was considerably lower, and soon after central banks had launched a massive, post-covid monetary stimulus, innocently observed, “The unknown consequences of record low interest rates, unprecedented levels of global monetary and fiscal stimulus and deglobalization are all adding fuel to the fire of awareness and adoption.” It did not comment on what a reversal of stimulus would do to the fire.

Fidelity responded to the DOL “serious concerns” release as to a torpedo in the stern. In a letter to Khawar, it asked him to withdraw the release. Among other points, Fidelity, which is exploring including other crypto assets in addition to bitcoin, took offense to DOL’s implication that the risks it cited applied to “all ‘cryptocurrencies.’”

The investment giant nearly boiled over at DOL’s warning that plan fiduciaries exercise “extreme care” when considering crypto. “The message is clear,” Fidelity noted like a wounded bear. “The Department views cryptocurrencies as imprudent investments for a 401(k) plan.”

I asked Fidelity if it believed that cryptocurrency has intrinsic, as distinct from speculative, value. No comment. I asked how crypto fits within the concept of the prudent man rule. It said, “We strongly encourage ERISA plan fiduciaries to consult with their ERISA counsel” (i.e., from a legal standpoint, not Fidelity’s problem).

But Fidelity, which plans to make bitcoin available in 401(k)s by midyear, is surely worried that the DOL release will cool the interest of sponsors. It has announced one client, the software firm MicroStrategy. MicroStrategy is run by Michael Saylor, a crypto enthusiast. The company owns 129,000 bitcoin (worth $3.86 billion), and Saylor has been touting its investment with comments such as “You can’t can’t (sic) stop buying Bitcoin.”

Fidelity is courting other potential adopters, but the effort has been chilled. “Plan sponsors who may have been interested in offering digital investments are less likely to do so because of” the DOL release, says Jennifer Eller, a principal at Groom Law Group in Washington.

Prof. Prasad had nothing but praise for the technical achievement of blockchain. He cited its record keeping, its improbable mix of public transparency and personal anonymity, its potential for effecting transfers without using bank intermediaries. However, he pointed out, the owner of a bitcoin does not own the technology. “All you own is a piece of code that only you can unlock with your key. The only reason it has value is everyone else thinks it has a value.”